Disclaimer: This guide is intended for general educational and informational purposes only, in conjunction with other resources on the subject. This guide does not provide legal advice or establish an attorney-client relationship between the reader and authors. Always consult an attorney together with competent tax and financial advisors regarding your specific situation prior to taking any steps.

Acknowledgments: We are grateful to Open Oregon State for their support in developing this handbook and making it freely available. We also thank Schwabe, Williamson & Wyatt for support in the development and wider distribution of this handbook at this critical time in Oregon agriculture.

We are also indebted to the colleagues who have worked on farm succession planning with us throughout the years and reviewed this handbook, providing thoughtful insights and suggestions. Our thanks go to Nellie McAdams, attorney, Oregon Agricultural Land Trust; Ashley Rood, farm preservation program director, Rogue Farm Corps; Matt Bisturis, attorney, Schwabe, Williamson & Wyatt; Maria Schmidlkofer, attorney, Schwabe, Williamson & Wyatt; Dave Buck, CPA, Aldrich CPAs and Advisors LLP; Sherri Noxel, OSU Austin Family Business Program; and Bart Eleveld, OSU Department of Applied Economics.

Christy Anderson Brekken, M.S., J.D., is faculty member in the Department of Applied Economics at Oregon State University, where she prepares the next generation of agricultural leaders to enter the field by teaching courses on agricultural law and environmental policy. Ms. Brekken has also developed and presented farm succession planning workshops throughout the state in collaboration with colleagues at Oregon State University. Her research includes The Future of Oregon’s Agricultural Land, a report on the transition of Oregon’s natural resource lands to the next generation. She holds a M.S. in Agricultural and Resource Economics from Oregon State University, and a J.D. from University of Minnesota.

Joe Hobson, J.D., is a shareholder at Schwabe, Williamson, & Wyatt with an office in Salem, Oregon. He has been practicing business and organization law for 40 years, with a focus on helping family farms, ranches, and forest owners in their business organization. Mr. Hobson has also been integral in Oregon’s agricultural landscape through his work with nonprofits and special districts that focus on agricultural interests. He was the Oregon Farm Bureau’s first general counsel, and helped to develop the Oregon Agricultural Education Foundation and the Oregon Agricultural Legal Foundation. Mr. Hobson has helped many Oregon family farms and ranches develop and implement their business organization and succession plans, and he now presents at workshops around the state to educate and empower producers to take the next steps to pass their legacy on to the next generation. He holds a J.D. from Willamette University College of Law.

Introduction to Farm Succession Planning

3

Every farm, ranch, nursery, dairy, or other agricultural operation is more than a business. It is a connection to family and tradition and provides essential food, fiber, fuel, and other benefits for society. But without attention to the farm as a business, it will not survive into the future or continue to provide those important connections and services. A farm’s management succession and estate planning are often uncomfortable topics for everyone involved. However, they are essential to protect and extend the agricultural operation.

Four Fundamental Goals for Farm Succession Planning

Preserving family relationships

Strengthening the farm business

Protecting owners and operators from business disruptions

Minimizing complexity and expense

The purpose of this guide is to provide foundational education for farm and ranch families on how to create a basic business succession and estate plan. In working with farm families, we have identified four fundamental goals for the farm succession planning process: (1) preserving family relationships, (2) strengthening the farm business, (3) protecting the owners and operators from business disruptions, and (4) minimizing the complexity and expense of succession and estate plans. With some basic knowledge, you will be educated consumers of legal and financial services, which may save you time and money as you consult with the attorneys, accountants, and other professionals who are key to creating a successful plan. This guide also gives you a starting point as you consider your alternatives and begin family discussions about the roles that each family member or nonfamily member may play in the future of the farm as a business.

Throughout this guide, the terms farm and farmland include ranches, dairies, nurseries, or other agricultural operations. Oregon agriculture is incredibly diverse, with more than 220 different products grown and sold across the globe, which is one of the strengths of the sector that is worth

preserving. Farm succession and estate planning are important for all agricultural operations. The information provided here will assume the farm is in Oregon. There are many differences among states when it comes to taxes and regulation. And though some of the specifics included here may not apply in other states, the basic motivation and planning steps are universal.

Business and Estate Planning Team

lawyer

accountant

financial planner

banker, appraiser

insurance agent

business succession consultant, family counselor, mediator, or succession planning training

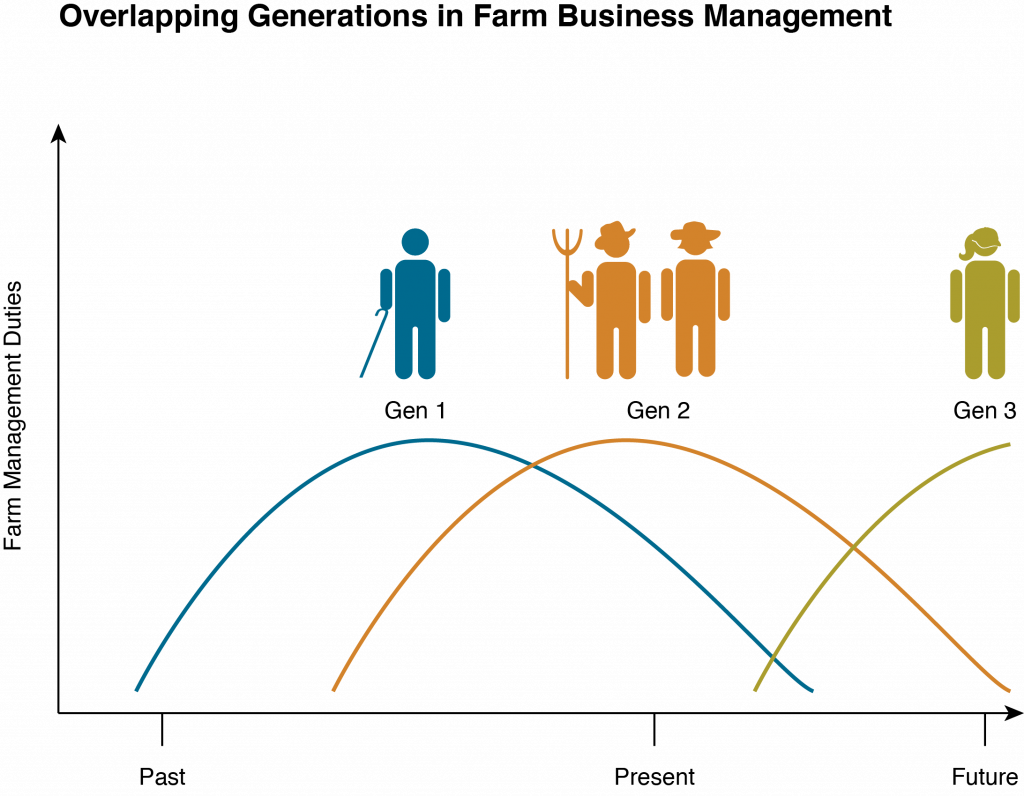

Throughout this guide, we will also refer to the three generations involved in the farm business (figure 1). Generation (Gen) 1 is the “grandparent” generation. Those in this generation are in their retirement age but often still own and may still be actively involved in the operation. Gen 2 is the “parent” generation. They may be actively involved in the farm operation and are planning for retirement soon. Gen 3 is the “child” generation. They are typically young adults who are in college or are recent college graduates and are determining a career path. It is also crucial to include the nonfarming family members in the business succession and estate planning because family dynamics are as important as the business balance sheets. Nonfarming family members can feel satisfied with the process by being included and receiving meaningful gifts that do not need to have the same monetary value as the business interests or gifts received by the farming family members. Everyone must feel included in the family legacy, but not everyone has to (or should) have control of the farm business.

Figure 1. Overlapping generations in farm business management

Today, many Gen 1 and Gen 2 farm owners and operators do not have a Gen 3 member in the family who wants to come back to the farm, so the owners may be looking for nonfamily successors to take on management duties. While an outright sale of the farm to a new operator might seem like the only option, it is often not in the best interest of the farm, the retiring generation, or beginning farmers. Management and ownership successions give the retiring generation a chance to pass on their knowledge and maintain long-term business relationships that benefit the farm and the new farmer in the long run. Management succession also allows the retiring generation to draw ongoing income from the farm rather than receive a lump sum in a sale, which may undervalue the farm as an ongoing operation. Likewise, many Gen 3s who are studying agriculture and agricultural business management in college today do not have a family farm to “go back” to, but they aspire to own their own farm. Because of land prices, student loans, and other expenses, buying a farm or starting a new operation outright is out of the question for young farmers without family land or significant capital. There are fruitful relationships that can be developed with nonfamily successors. We will pay special attention to the considerations of nonfamily succession planning for both Gen 2 operators considering including a nonfamily Gen 3 individual in their business succession plan and potential nonfamily Gen 3 successors.

Whether the incoming generation is family or not, business succession planning requires a clear articulation of shared goals and plans, immaculate documentation, and attention to detail. When expectations and plans are well defined, people can feel secure about the future of the business and their place in it. It is sometimes assumed that a succession plan will unfold naturally as the generations work together to manage the farm, but it is important to create expectations and plans that everyone agrees to abide by. Clarifying roles and responsibilities does not imply that the elder generation distrusts the younger generations; rather, early planning can give everyone clarity, confidence, and increased family harmony. It also opens lines of communication so that if circumstances change, there is a basis for reopening the conversation and changing the plan.

Bringing a new generation into the operation means new skills, ideas, and labor that are assets to the business—and more people that need to be paid out of the business returns.

It is also critically important that the farm business is viable, meaning that it is generating a reasonable rate of return as an ongoing agricultural operation. It must have value and the potential to continue to create income for the owners and operators into the future. By bringing a new generation into the operation, you are bringing in new skills, ideas, and labor that are assets to the business. However, you are also bringing in more people that need to be paid out of the business returns. The goal of a successful succession plan is not to give more people a smaller slice of the pie but to make the pie bigger (figure 2). That goal needs to be a key element in the planning process so that the incoming generation has a living wage and the retiring generation can take out money for their household and healthcare needs after they leave the day-to-day management of the business. A business can become stronger through the focused attention and development required in a succession planning process.

Figure 2. Increasing farm income for succession planning

While the goal is a successful business succession, which allows Gen 2 to retire and Gen 3 to enter farm business management, things do not always go as planned. Agricultural businesses face many risks, such as increases in the cost of inputs, decreases in farm product prices, natural disasters, changing regulations and trade relations, family illnesses, legal liabilities, interest rate changes, land development pressures, and others. The goal of business succession planning is not only to strengthen the business but to protect the people and assets involved in the business if things fall apart. For example, if one of the farm’s business lines is hit with a devastating shock, the land and other assets need to be protected. Just as buildings in an earthquake-prone area are built to withstand the shock or fall apart in a way that protects the occupants, we must create a business plan that protects valuable assets that are necessary for the farm and provides a road map for sorting out the various and sometimes competing interests of the family members if a shock hits the farm.

Finally, we want to create a plan that is manageable for the people who are living with it. While the structure will likely be more complex than a sole proprietorship, the administration of the plan must be understandable and sustainable so that the people involved can go about running the farm, not managing the business structure. The same can be said for other aspects of estate planning, such as managing taxes and trusts. While we plan to minimize taxes, the strategies cannot be so complex that they are unmanageable or create other types of risks. We can use common, existing tools for planning and develop relationships with trusted professionals, such as an attorney and accountant, who help the farm owners keep things on track.

This guide is organized to give you an overview of how to pass the family farm on to a new generation. The goal is to preserve family relationships, tune up the farm business to be successful today, smoothly pass the farm to the next generation as the current operators retire, and take care of the whole family when the older generations pass away. There are five distinct but interlocking pieces to this process: (1) take care of the family, (2) ensure the financial health of the business, (3) organize the farm business limited liability company (LLC), (4) organize the farm LLCs for the business succession plan, and (5) create the estate plan. All five steps can happen simultaneously in the planning process or can be picked up and revised at any time as circumstances change.

Step 1—Take care of the family

We are focused on the nuts and bolts of business succession and estate planning, but the purpose of all of this is taking care of your family. Generations have built up your family farm, and you have a legacy to pass on to today’s and tomorrow’s generations. If you are Gen 1 or 2, start by letting your family know that you are thinking about what will happen to the farm and family after you retire or die and that taking care of them and the farm is your priority. It’s never too early to start! Thinking carefully about your goals, who will manage the farm, and your family’s wishes will be the foundation for conversations with your estate and business lawyers. If you are Gen 3, you will want to communicate your commitment to continuing the farm legacy and your timeline and open lines of communication about management succession.

The future of your family and farm is the best motivation for getting started, and getting started immediately may inspire you to move deeper into the planning process. Every family is unique, and you are the only one who can begin your business succession and estate distribution plan.

Step 2—Ensure the financial health of the farm business.

Ensuring business viability involves the analysis of the business’s income, rate of return, operating capital, and risk management. In this process, managers may need to change aspects of the farm to increase the rate of return to accommodate incoming generations. We recommend increasing the rate of return because the goal of business succession is not to give more people a smaller slice of the pie but to make the pie bigger in the planning process. A strong business is a candidate for a successful business succession process, and the business can become stronger through the focused attention and development in the business succession planning process.

Step 3—Organize the farm business limited liability company (LLC).

While planning to improve the farm’s financial position and risk management, you will work on getting the farm business organized in such a way that it will facilitate the succession plan. We will discuss legal business entities and how to organize a business for optimal risk management in the present, regardless of whether the business succession plan is put into action immediately or in the next decade.

Step 4—Organize your farm LLCs for your business succession plan.

Next, you will develop a business succession plan for the farm, with the estate distribution plan in mind. This will involve business organization steps building from the foundation established in step 3. The succession plan establishes the timelines, milestones, and processes for bringing Gen 3 into management and then ownership of the farm while Gen 2 retires.

Step 5—Create the estate plan.

The business succession plan gives Gen 2 peace of mind, knowing that the farm will continue on as a legacy of their hard work. We circle back to the distribution plan created in step 1, using legal tools such as wills and trusts while planning for taxes and other expenses that can threaten the value that you want to pass on to your family.

We finish this guide with some general observations on how creating your business succession and estate plan can help the farm and family weather common disruptive life events, such as death, divorce, debt, and other risks. The ultimate goal is to provide all family members with realistic expectations and peace of mind, knowing that everyone’s unique interests are considered during some of life’s most challenging times.

Chapter 1: Take Care of the Family

Gen 1 and 2 (and generations past) built the farm to take care of the family. While we are focused on business succession planning, the ultimate purpose is to keep the family together. A good business plan can minimize family tensions by setting up clear roles and expectations, clarifying the business relationships to allow the family relationships to thrive. A good estate plan ensures that everyone is treated equitably, not necessarily the same or equally, because each family member is unique.

Prior to setting up business entities and estate planning, it is important to have open, honest conversations with family members. It starts with letting everyone know that you are thinking about the long-term operation of the farm after you retire or die, and it is never too early to start those conversations. Even new farmers should think about what will happen to the farm and family if the unthinkable happens. You can share your goals for the future of the farm and find out what family members want in their relationship to the farm.

We also start with the family because the business succession plan needs to be driven by Gen 2’s estate distribution plan, which is the outline for who gets what when Gen 2 (and/or Gen 1, if applicable) passes away. This means that you should consider your broad estate planning first. To develop a distribution plan, Gen 2 should create a list of all their personal and business assets alongside a list of everyone who will get a bequest. At this point, it would be a broad outline, such as “The most important thing is for the farm to pass on to the next generation when I die,” “I want child A to end up with the farm,” “I want child M to get the china and child N to get our wedding rings,” or “I want to leave a donation to our church.” A distribution plan doesn’t need to be much more complicated than that at this point. This is a good time to talk with your family to find out which gifts will be meaningful or helpful to them. Don’t assume you know what your family members truly want! These conversations can be very illuminating for many families. The best way to honor your family members is to give them gifts that are meaningful. Giving individualized gifts recognizes the special relationship you have with each member of your family.

This is a great time to sit down and start your estate distribution plan because it can proceed without any more instructions. The future of your family and farm is the best motivation for getting started, which then may inspire you to move deeper into the planning process. Every family is unique, and you are the only one who can begin your estate distribution plan.

You should also be actively engaged in finding a Gen 3 successor from within or outside of the family. The lack of a family successor is a major stress for many of today’s farms. Today, the average age of Oregon farmers and ranchers is around sixty years old, and many do not have a family member in the next generation who wants to come back to manage the farm. Hence, finding a nonfamily successor is becoming necessary for many farms. Meanwhile, many young people are training to go into agriculture but do not come from a farming family and are looking for opportunities to enter a career in agriculture. Preparing your family for a nonfamily successor is an important conversation. You may also work with multiple potential successors until you find one that is right for the long term. Your potential successor may start out as an employee, move into management duties, take over management, and finally take ownership interests in the farm. You will want time to find and train potential successors until the right person comes along, understanding that not everyone who trains with you will work out.

Finally, getting an idea about your goals, your successor, and your family’s wishes will be the foundation for conversations with your estate and business lawyers. Your goals for the future and your family’s expectations will impact the way you structure your business organizations, succession plans, and estate plans. As you go through this process, expect that it will take significant time, effort, and expense. It’s a lot cheaper to work with your family by hosting family meetings or participating in farm succession trainings than it is to work out all of these details in your lawyer’s or accountant’s office. By starting the process with your family, armed with knowledge about your options, you will save time and money in the long run.

Step 1—Take care of the family by gathering ideas and expectations.

Let everyone know that you are thinking about the long-term operation of the farm after you retire or die.

Talk to your family about your estate plan. Find out how family members would prefer to be recognized in your estate plan. Start establishing expectations about the business succession and estate plan well before it is drafted.

Discuss farm succession with family members who express an interest in managing the farm to assess their level of commitment and expectations and involve them in the decision-making process.

If you do not have a Gen 3 successor in the family, seek out Gen 3s that would be a good fit by networking with other farmers, connecting with local or state agricultural education programs such as those at Oregon State University, or connecting with other organizations that manage farm training or young farmer programs.

If you do not have a Gen 3 successor, set up an internship or limited farm manager position as an introductory period with no long-term commitments. You may need to work with several potential successors before you find the right fit. Use the process to plan and practice turning over management tasks to as well as training an incoming Gen 3.

Identify professionals that can help you through the process. Start with any professionals that you already work with, ask for referrals if you need to find other experts, and get advice from lenders and other farmers.

Attend a business succession workshop or seminar and explore further business succession resources.

Chapter 2: Ensure the Financial Health of the Farm Business

The second step in the business succession planning process is to evaluate and tune up the farm’s financial situation. We will accomplish that through an analysis of the farm’s ability to support multiple generations during the transition process. We will review the farm’s income needs, value, rate of return, operating capital, and risk-management strategies.

A. Farm Business Financial Viability

The first piece of business succession planning is making sure that the farm business is currently economically viable with a reasonable rate of return and developing a plan to expand the business so that it can support both the new generation and the retiring generation. The retiring generation has worked their whole life to build the business and should expect the business to continue to support them into retirement. The new generation brings new skills, ideas, and labor that are assets to the business, but they also need to be paid out of the business returns. The goal is not to give more people a smaller slice of the pie but to make the pie bigger in the planning process. A successful business succession process starts with a strong business. The business succession planning process should include making the business stronger as well.

1. Determine the Farm’s Income Needs

A financial planner and accountant can help you prepare for retirement through budgeting household income needs and understanding retirement accounts, pensions, Social Security, Medicare, and other sources of income and support.For a viable working farm, a substantial part of the family’s household income is coming from the farm. Most farms also have off-farm income from a spouse, which may also provide medical or other insurance. When Gen 2 retires from operating the farm, their expenses will change. If a spouse with an off-farm job retires, that will reduce the family income and add new expenses, such as medical insurance or others. When Gen 2 retires, each person may draw from Social Security, retirement accounts, or pensions from off-farm jobs to supplement their income. Their tax situation will also change with a decrease in income and no business deductions for on-farm housing or business vehicle expenses. Retirement brings big financial changes, and Gen 2 will have to carefully budget the farm income to provide for their own retirement in addition to Gen 1s who are still supported by the farm. A financial planner and the family accountant can be extremely helpful in preparing for retirement, from budgeting to understanding retirement accounts, pensions, Social Security, Medicare, and other potential sources of personal income or support and expense.

The incoming Gen 3 operators may also have an off-farm source of household income but should also be able to expect the farm to provide a substantial part of their income, especially as they start a family and that family grows. If Gen 3 becomes the new farm operator and moves to the farm, housing costs may be required to support a new household, whether that be adding housing to the current land or one generation moving into other housing. Gen 3’s household budget likely looks different from Gen 2’s budget and requires a fair market wage from a viable farm business.

It is essential to recognize that the farm will be expected to support more people in the future, which will require a fair accounting of the farm’s current value, the rate of return on farm assets and cash flow, and the other assets owned by Gen 1 and Gen 2 that can provide for their retirement. The succession planning must consider how farm assets can be managed in a way that supports both Gen 1’s and Gen 2’s retirement needs—which may come from the farm income—Gen 3’s household income needs, and the farm’s ongoing capital and cash flow needs. An honest accounting will show that the farm will have to increase its income in order to support all of these objectives, which will make it a stronger business (figure 3).

Figure 3. Increasing farm income for succession planning

2. Determine the Farm’s Value

It is critical to find out what the farm is worth and the farm owner’s total assets. This inventory is useful for business valuation, estimating estate taxes for further planning, and understanding everything that is available to include in the estate plan, which provides for meaningful gifts for all family members whether or not they plan to be involved in the farm business. To create an estate plan for the business owners, we also must inventory their personal assets.

A farm is a business. A business is worth what you can sell it for. A sale of a business is based on the value of its assets: real property, personal property, and the business’s value as an economically viable unit. An agricultural business with its own brand, such as a successful winery or a processed-foods company, may have additional value due to its brand name, future contracts, and reputation. A farm’s financial performance must promise the safety of capital contributions and an adequate return. Otherwise, the operation is only a speculative economic unit, not a secure financial investment for the incoming generation. Here we will look at the present value of the farm, and in the next section, we will address its rate of return.

For the most part, the only asset typically used to value a farm at any given point in time is the land, timber, or other land-based assets because equipment and other property depreciate quickly. Livestock operations, such as dairies and cow-calf operations, also have notable value in the herd. If the farm is already organized as a business entity (an LLC or corporation), the value of the business should be determined based on what the business owns. However, because the vast majority of Oregon’s agricultural businesses are still owned as sole proprietorships or partnerships, the land, equipment, livestock, and other assets are technically owned by the operators personally. To organize the business, we must inventory the business assets.

With respect to the land, we want to know how much there is, where it is located, and the current fair market value. We also want to know whether it is owned or rented. Quite often in today’s modern farming operation, less than half of the land being farmed is owned by the family doing the farming. For the land that is owned, we want to know how much that land is worth on a true fair market basis. In other words, if a piece of the land was put up for sale today, how much would a willing, knowledgeable buyer actually pay for it? The assessed value is often not the best measure of the current value; the best way to determine true market value is to use comparable sales in the area rather than a formal appraisal. Often a knowledgeable realtor in the area can help by providing an estimate of what the land can be sold for at its present market value. Such an estimate is generally called a comparable market analysis.

Farmers have to buy and operate a large amount of very expensive equipment because of the increase in productivity that the equipment brings to the operation. However, farm equipment begins to depreciate in value the moment it is driven away from the dealer. Investments in the latest equipment dwindle very quickly. In valuing livestock, we consider herd size, value, and the method used to keep track of animals as they come and go through the operation. For example, dairies often have herds of registered cows with certification of their genetic background. This makes a cow more valuable, and the reputation of the farmer becomes a part of the value of the animal. Each animal typically has a brand or ear tags to identify the background of the animal and its place of origin and to and distinguish it from the other members of the herd. For purposes of succession planning, auction houses in the area can help by providing an estimate of the sales price of equipment and livestock.

The farm owners may have other assets owned in their name, such as investment accounts (individual stocks, bonds, or mutual funds), cash or cash equivalents (checking accounts, savings accounts, money market accounts, certificates of deposit, etc.), security deposits, retirement accounts (401[k], IRA, SEP), annuities, life insurance, and other personal property such as vehicles, boats, airplanes, collectibles (value to a knowledgeable collector), and other personal property (valued at a farm sale or garage sale). In order to accomplish a successful succession plan, the professionals will need to know about and take into consideration all of these assets.

3. Calculate the Farm’s Rate of Return

You will want to calculate the farm’s rate of return to determine if the business is currently economically viable. Then you will have a baseline for developing a plan to expand the business so that it will have a reasonable rate of return to support both the new generation and the retiring generation. You will gather this information for your own business planning purposes if you are not already doing it regularly.

The most valuable asset of a farm is the land. The value of livestock is also a major asset for dairies and cow-calf operations. The rate of return for a farm’s land or livestock is the net gain or loss on the investment in the asset over a specified period, expressed as a percentage of the original investment. Gains on investments are defined as income received plus any capital gains realized on the sale of the investment. Although you are not planning to sell the assets, you will pick a date to calculate the rate of return on assets that you hold over a reasonable period. For ease of illustration, we will use a one-year period as an example. To calculate the rate of return for the land and/or the livestock over a one-year period, first determine the amount of the original investment in those assets. Next, determine the fair market value of those assets at the beginning and at the end of the most recent year. Next, calculate the net excess income (profit) or loss received from the farming operation that is using those assets to generate income. Net excess income is the amount that exceeds or falls below operating expenses excluding salaries, distributions, or draws paid to the owners.

For simplicity, let’s say the original investment in the asset was $100,000. The difference in the fair market value of the assets at the beginning of the year and the end of the year was $4,000 (capital gain), while the operation enjoyed the net excess income of $3,000 during the year. Add together the gain in value and the net excess income for the year, which comes to $7,000. The annual rate of return on the investment for the one-year period is the increase in value plus the net excess income divided by the original investment in those assets. To calculate the rate of return from our example, the original investment is $100,000, the increase in value plus the net excess income is $7,000. Thus the annual rate of return on the investment is 7 percent ($7,000 / $100,000 = 0.07 = 7 percent; table 1).

Table 1. Rate of return on land example

Capital Gain Year 1 (Market Value)

Value End of Year

$104,000

–

Value Start of Year

$100,000

=

$4,000

Net Income Year 1

Revenue attributed to land

–

Costs associated with land

=

$3,000

Total Return Year 1

Capital Gain

$4,000

+

Net Income

$3,000

=

$7,000

Rate of Return

Total Return on Land

$7,000

/

Value Start of Year

$100,000

=

7%

This example should demonstrate that a key part of determining whether a farming operation is a viable business is the net excess income being generated by the farm. Capital gains from increased asset values are not “realized” at the end of the year because you do not sell them. The farm continues to own them to generate income. The increased value of the land and cattle is locked in until they are sold; that value cannot be used by present operators to pay expenses or for the kids’ college tuition unless you convert that asset to cash, which comes with risk and will be discussed later. Therefore, it is crucial to focus on generating adequate net excess income from the business when planning a farm succession.

For a farm that is an ongoing business, the gain in value of the hard assets (land and livestock) will hopefully be passed down to the next generation without ever being converted to cash or diminished. Whether that happens will depend in large part on if a successful business succession plan coupled with a well-designed and coordinated estate plan can be developed for the farm. It will also depend on whether market conditions and public policy are generally favorable or unfavorable to the farm over time.

For a farm to be a viable business, its rate of return must be equal to or greater than what you could expect to receive in fair market rent for that same asset under a triple-net cash lease, meaning rent payments minus taxes, insurance, and maintenance and adjusted by any mortgage payment if the land is not owned outright (table 2). In other words, in order for a farm to be a good prospect for succession planning, the farm should be making more money through the current or projected farming operation than it could make by renting the land and cattle out to another operator. The income generated from the land must cover all land expenses and then some to show a profit.

Table 2. Triple-net cash lease calculation

Real Estate Taxes

+ Property Insurance

+ Property Maintenance

+ Mortgage interest (if any)

= All Land Expenses

+ Expected return on land (2%-5%)

= Minimum Annual Rental Payment

4. Increase the Rate of Return

For a farm operation to support the next generation, it is likely that the farm will have to increase its rate of return on investment, generating more farm income that can be paid as retirement income to Gen 2s and household income to Gen 3s. As discussed, the key goal is to increase the net excess income from the business so that it can be paid as wages, bonuses, and benefits or reinvested in the business for future growth.

Each farm has its own unique path to increase the rate of return and thus requires a careful analysis of its current operations and future opportunities. However, there are a few general ideas to increase rate of return for current operations.

First, diversify the farm by finding new markets that pay higher prices for the products. Diversifying the farm’s activities provides for different streams of income and expenses, which can also provide some risk management if markets change. This may come in the form of different marketing channels, such as going directly to retail, restaurants, schools, hospitals, or consumers.

Ideas for increasing rate of return for your operation:

Diversify income streams through new markets, value-added processing, or certifications.

Reduce cost of production after analysis of expenses or investing in new technology.

Increase productivity by adding land, higher-value crops, or new business lines.

Markets for local and regional foods, which could be anything grown in Oregon, often offer price premiums. Products can also be differentiated by certifications, such as USDA-certified organic or other third-party certifications. Food processors in the region seek out certified organic products, and there is still higher demand than supply for products such as organic grains and nuts. There are also niche products, like specialty grains, that are in demand. Finally, some on-farm and value-added processing can allow you to sell products at higher prices. However, with all of these opportunities come costs and risks, and the prices obtained must be higher than the costs associated with the differentiated products or markets. Some have high fixed costs, such as the three-year transition time to organic and certification fees, but if the costs can be covered in the long run for a consistently higher rate of return, the investments will be sound.

It’s not a value-added product until I sell it and am paid for my efforts. Before then, it’s cost added.

—Oregon farmer, pickle and jam producerAnother way to improve the bottom line while continuing with current production requires lowering the cost of production, which accountants refer to as the cost of goods sold. The first step is tracking your costs and returns for different farm business activities. If you have not moved beyond paper and pencil accounting, organizing your financial information using basic business accounting software or starting a relationship with an accountant is highly recommended. It will take time, effort, and money to get started, but it will save you headaches in the future and give you valuable information about managing your farm costs, revenues, and the economic viability of various crops or other business activities. You will have a clearer picture of which costs you can control; many costs of production, such as fuel, seed, fertilizer, pesticides, and other inputs, are outside of your control unless you switch practices. Labor costs are also dictated by federal and state laws as well as labor market forces, although some types of agricultural labor are also exempted. Many farms are investing in mechanization to avoid the cost and risk of employing labor. Equipment is also expensive, including new technologies. Sharing equipment through rental agreements or hiring custom-cropping operations could be a way to decrease your investment in equipment. Overall, new technology such as precision agriculture and mechanization can help farms control their input and labor costs, but there are still up-front and ongoing costs to be considered. Some of those up-front costs can be recovered by participating in USDA or other subsidy programs that share some of the cost of improvements, such as renewable energy or other conservation technologies that both reduce some costs of production and have environmental benefits (see “Resources” section).

Finally, a farm can increase productivity to improve the rate of return. Productivity simply means the rate at which you produce a unit of output (e.g., a bushel) per unit of input, such as land and labor (e.g., acre or person-hour). Increasing productivity means producing more income without increasing your current resources. Some of the ideas already discussed increase productivity, such as switching to higher-value crops on the same land or mechanizing aspects of your operation. Other ways to increase productivity are to add more land, which is a challenge in Oregon because of the high competition for agricultural land and a limited supply. Adding land increases productivity if you can use your current equipment and labor to work the extra land, increasing output overall (but be aware of the rate of return on the new land to be sure it is worth the investment). Oregon is also challenged by the availability of water and presence of wetlands in many areas, which are highly regulated—but getting the ability to irrigate your land or add drainage could also increase the productivity on the land you own. You can also add recreational opportunities such as agritourism or other limited public access for a fee. Again, be aware of regulations and legal and financial risks associated with inviting the public onto your land, but the benefits can outweigh the costs for some operations.

In addition, organizing your business to better handle risk and improving the chances of getting paid for your product—which are discussed in the following section—will benefit the business and your rate of return in the long run.

5. Value and Incorporate Gen 3 Skills

The incoming Gen 3 will bring valuable skills and experience to the business, which can foster new business viability options such as the ideas previously discussed. Many family farms require their Gen 3 children to get a college education and experience in a different job before they decide to come back to the farm and begin the process of taking over management duties. Seriousness and experience are invaluable aspects of a competent Gen 3. Nonfamilial Gen 3s are also getting farm management experience, creating a strong crop of young farmers who are eager and dedicated to taking over a successful farm operation. Many Gen 3 graduates studied crops, soils, horticulture, animal science, and other valuable programs. However, to manage a complex farm business, it is imperative that Gen 3s also take courses, or an entire degree program, in agricultural business management, microeconomics, accounting, legal issues, and other business topics as applied to agriculture.

As part of the business succession plan, we recommend that Gen 3 individuals manage a separate business line, bringing in new assets and skills. The succession plan can allow for some independent decision making as well as overlap between the retiring Gen 2 and the incoming Gen 3. The business succession plan can be designed to reach the simultaneous goals of increasing farm rate of return and income, strengthening the farm business, and fostering the management skills of the incoming Gen 3.

6. Increase the Operating Capital

A business is only viable if it generates excess cash after deducting the cash flow necessary to cover its expenses when they come due. For a farm business, there are high expenses at the beginning of the crop year. During that time, cash flows out to plant and tend the crop and keep the lights on. Payment comes after a crop is harvested and might need to be cleaned, processed, and stored before it can be delivered to the buyer and payment is due. Often, expenses for the new crop season are paid before income from the previous crop has been received. The money that flows out during the crop-year expense-income cycles is operating capital. Many Oregon farms now require millions of dollars of operating capital to bridge the gap between the time when expenses have to be paid and the time when income is received for the next crop.

Farm lenders are key partners in providing operating capital, typically in the form of a line of credit. The number of agricultural lenders is shrinking in Oregon, and operating capital can be hard to come by for some farms. Most operating loans or lines of credit are short-term variable interest loans that take the farm’s equipment, products, and accounts as collateral, putting the farm at risk if income does not come in as expected and the loan is unable to be paid (known as secured debt, security interests, and secured transactions, with the lender filing a financing statement / UCC-1; this is different from a loan using land as collateral, which is a mortgage). While lenders that work with farms understand the farm expense-income cycle and can negotiate loan terms, it is prudent for farms to develop their own sources of operating capital, which can also cut down on interest payments and improve the rate of return, reduce risks associated with debt, and improve business viability.

To the extent possible, any net profit from an operating year can be saved by paying down debt with high interest rates or putting the money into investment accounts that offer a reasonable rate of return. A highly liquid account that you can draw on anytime, such as a standard savings account, will earn a much lower interest rate than a money market account that requires a high minimum balance or a certificate of deposit that must stay in the account for a number of years. Excess income can be invested in stocks or bonds to grow over time and can be sold at any time if necessary but with higher risk. Creating pools of liquid assets that can appreciate over time will build an operating capital fund for the future.

7. Convert Farm Assets into Retirement Income or Operating Capital

If you calculate retirement needs of Gen 2, family income for Gen 3, and operating capital to continue as a business and determine that the farm business does not generate enough excess income to meet those needs, then the temptation is to convert some of the ownership interests in the land or other assets into cash through sale, lease, easements, or expanding ownership to more people who contribute capital to keep the farm running. This is a precarious position for a farm and may indicate that the farm business is not viable as operated. Any of these steps to convert farm assets into cash should be done with the utmost care, and cash received should be directed toward investments to sustainably increase the rate of return, because these steps can be irreversible and may lead to the end of the operation. There are several options to consider, with caveats:

Sell land with leaseback and option to repurchase. Land can be sold, generating cash for the business to pay down debt. Reducing the farm’s debt load avoids interest payments, and additional cash from the sale of land can be added to the farm’s reserves to reduce the need to borrow operating capital. In negotiating the sale, the terms will include the right of the farmer to lease the property back from the new owner on a written farm lease. The terms of the lease should allow the farming operation to reach financial viability—for example, a fixed term (e.g., five years), automatic renewal when the term expires, and the amount and timing of lease payments. The sale and lease agreements should also give the farmer a “right of first refusal” if the new owner decides to sell and an “option to purchase,” allowing the farmer to buy back the land if the financial position of the farm allows. Using these kinds of provisions, the transaction can be made reversible, allowing the farmer some ability to pay down the debt or create savings.

Sell equipment with leaseback and option to repurchase. The same contract terms can be applied to the sale of equipment to generate cash to pay debt or build operating capital, with the same caveats. However, equipment will depreciate over time, which can impact the price and desirability of buying the equipment back if significant time passes. It could be a short-term bridge to produce a smaller amount of operating capital if necessary.

Sell aneasement. An easement is a voluntary agreement between a landowner and an authorized organization like a land trust or a soil and water conservation district to permanently limit some of the development or use rights on a property. Conservation easements may apply to all or just a portion of the property and need not require public access. Working lands easements are conservation easements that allow farmers and foresters to continue productive farming and forestry operations and keep the land in production forever. Farmers may also enter a conservation easement, which is a promise to not farm a particular parcel that is ecologically sensitive, such as land next to a river, wetlands, or a habitat for critical species. Farmers in Oregon have also developed wetland mitigation banks that restore historical wetlands in exchange for payment from developers that seek permits to destroy wetlands in another area, which is a program managed by the state. The easement holder, which is typically a land trust or government agency, is responsible for making sure the easement’s terms are followed.

Easements may allow landowners to continue to own and use their land, sell it, and pass it on to the next generation. The farmer may get the payment when they enter into the easement or at regular intervals, depending on the terms of the agreement. For easements “in perpetuity,” with no end point, the appraised value of the land is reduced because future owners also will be bound by the easement’s terms, although the easement does not necessarily affect sales price where the agricultural value of the land is high. Besides generating capital for the business, an easement can have income and estate tax benefits through deductions if the easement is donated (if applicable) and through reducing the total value of the land. We will discuss taxes in more detail later.

A farmer should exercise caution in entering any easement, whether an access easement with a neighbor or a family member or a conservation easement with a land trust or a government entity. Easements are complex documents and must be drafted carefully with true expertise and an eye toward making sure that the burden and business risk on the land and farming operation are what the farmer is expecting. Entering an easement adds complexity to management, as the easement holder will annually monitor compliance with the easement document. The easement agreement can be fairly detailed, depending on its purpose. Before entering into an easement on farmland, a farmer should seek competent legal, tax, and investment advice, form a relationship with the easement holder, and talk with others who have entered into similar easements.

Sell an equity position. The riskiest option is to sell an equity position in the farming operation, which brings in new owners who will contribute capital. It is crucial to get the help of an attorney and tax accountant with this path because it requires business reorganization and can have serious tax and securities law implications. Including a new partner in the operation can have a big effect on business decision-making going forward. While you can negotiate the rules about how business decisions are made, no amount of documentation can serve as a replacement for two partners who get along, communicate well, and have worked out a way to operate the farm as partners. Unless you are uniquely blessed with that kind of a relationship, you should avoid bringing in new business owners for the purpose of raising capital.

B. Managing Risk for the Health of the Farm Business

Any business is risky, and farming is a business. Farms’ risk-management needs are broad. Farms face risks from natural systems, such as droughts or floods that can devastate a crop and impact contract or loan obligations. Farms manage natural resources and as a result are subject to local, state, and federal environmental laws that may apply. Agricultural businesses typically use machinery and equipment that can be dangerous to workers or other people. Farms face a range of risks by taking on employees and must follow all employment laws, find and retain skilled employees, and set up ways to handle accidents or injuries. Farms often create off-farm impacts—such as smell, noise, dust, or chemicals—that cause neighbors to complain. Many farms have interactions with the public, selling products directly to consumers or inviting the public onto their land. Some farms maintain certifications that increase the value of their product but can be lost through mismanagement or due to natural or human forces that contaminate or damage their crop or infrastructure. Business risk is increasing every day with new markets, new rules and regulations, more development in rural areas, and new interactions with other industries. No one can make business risk go away. But it can be managed using some basic legal and financial tools.

1. Obtaining Insurance to Manage Risk

In this section, we will discuss using limited liability business organizations as an umbrella that covers general business risk. But even with an LLC or a corporation, the farm should have adequate insurance to cover liability risks from someone being hurt while on the property, by farm vehicles, by product contamination, by crop loss, or by other insurable risks. As described later, an LLC only limits legal claims to business assets; it doesn’t shield the business from all claims. You still need insurance to protect business assets. Adequate liability insurance will cover court costs and some expenses, protecting the business assets.

An insurance policy is a contract. You pay insurance premiums over time, and the insurance pays out in the event that one of the covered risks occurs. The covered risks are either for general categories of items or people such as “inventory” or “employees” or for specific things such as buildings and equipment. There are also limits to the amount of money that can be paid for damages to covered items, and often there are deductibles on claims so that you pay a limited percentage and/or maximum amount of the claim. Claims must also be filed according to the procedures in the policy, such as providing particular information within a certain amount of time after the event. Know what you are getting with your insurance and comply with the terms of the policy. Farm insurance can be expensive because farm activities are risky, so know what you want to cover, shop around, and work with your agent, who may visit your property and give recommendations.

When deciding on insurance coverage, first you should assess the risks on your farm that can be covered. Then choose insurance options for addressing the farm’s risks, such as property damage; injuries to visitors, customers, or service providers on your land; worker injuries; crop and livestock damage; and retail and wholesale sales liability.

Property insurance covers damage to structures, equipment, and inventory on your farm from weather events, fire, and theft and can also cover damage from other events such as loss of electricity. Make a list of the property that you want to cover and its replacement value when shopping for insurance and make sure to update your policy if you get new items or make improvements to be sure that everything is covered.

Property insurance often comes with liability or casualty insurance, so that if someone comes onto your land and is hurt, the insurance company will handle the defense of any lawsuit and pay damages, up to the limitation amount. If the cost of the injury is greater than the insurance limitations, then the farm is on the hook for the balance. Of course, higher policy limits come with higher premiums, so you have to make decisions about how much insurance you want to carry. If you are doing on-farm events such as agritourism or off-farm activities such as farmers markets or selling products directly to retailers or consumers, your farm liability insurance must have “endorsements” to specifically cover those events or an additional policy that covers product liability.

States require businesses to carry workers’ compensation insurance if you have any employees and impose fines for not having the insurance. Rates are based on the riskiness of the work that employees do. And it’s just a good idea, because farm work is very physical and insurance is a great risk-management tool. Workers’ compensation insurance covers any injury to an employee that arises in the course of employment, so anything from repetitive stress injuries to broken bones that happen on the job is covered. Cover everyone who works for you, from regular employees to interns, to make sure that all potential injuries are accounted for.

Crop and livestock insurance covers losses from natural disasters and is available from local insurance agents who sell and service federally subsidized crop insurance policies for many different types of operations. The USDA Risk Management Agency has resources to review different types of policies.

Insurance is an essential part of farm risk management. While the likelihood of catastrophic events may be small in any particular year, the magnitude of the cost to your business could be devastating. Carrying the right kind and amount of insurance depends on your farm operations and your risk tolerance. Working with an agent, you can create a farm liability insurance package that includes all the necessary components to minimize the impact of catastrophic events.

2. Managing the Risk of Not Getting Paid

Farms are also at risk of buyers backing out of contracts or not paying after delivery of products, especially if they sell perishable foods like fruits and vegetables. There are legal tools that you can use to get paid if a buyer backs out or goes bankrupt. These can be difficult rules and laws to navigate. The first step is to get help creating written contracts that protect your interests. They can be used for the types of transactions that you typically engage in and new business lines that you might begin.

Know which laws can be used to your advantage based on what you produce—for example, Packers and Stockyards Act (PSA), Perishable Agricultural Commodities Act (PACA), or state laws such as agricultural and landlord’s liens and those providing some protection for payment under production contracts. Some of these require basic language in a contract or lease; others require action on the part of the producer if they are not paid. Determine which laws are applicable to the products you sell, create basic contract or lease language, use it consistently, and keep the information on hand; it will save time and effort if you are in a situation where you don’t get paid in a timely manner.

Step 2—Ensure the health of the farm business.

Determine the income needs of retired Gen 2s, the income needs of Gen 3s and their family, and the farm’s cash-flow and investment needs.

Determine the farm’s value by making an inventory and an estimate of the value of each item. Also inventory nonfarm assets for estate planning purposes.

Evaluate the rate of return to determine if the farm is generating enough income to cover the income needs of Gen 2s and Gen 3s, and the farm’s cash-flow and investment needs.

Make a business plan to “make the pie bigger,” if necessary. Your prospective Gen 3s can make a business plan and budget to evaluate a new business line or expansion, for example. Planning to grow the business is a good way to involve Gen 3s and to assess their skills, provide training and experience, and give a sense of ownership over their role.

Consider options for converting farm assets into cash for operating capital or new farm investment, such as conservation or working lands easements. Remember that some tools can have multiple benefits, such as reducing the market value of the land for estate tax purposes. Other tools come with risks. All must be approached with caution and careful planning.

Take all appropriate legal steps to manage risks involved in the farm activities that you undertake in your business, from obtaining the right insurance coverage to drafting contracts, filing liens, and invoking other statutory protections when necessary.

Work with your accountant and other business planning professionals as you make business decisions.

Chapter 3: Organize the Farm Business Limited Liability Company (LLC)

When organizing a business, the first thing we talk about is risk. Every business can and should use legal tools to manage risk by limiting the liability of the owners for the acts of the business. Tools include separate business entities, proper and complete insurance coverage, complete and well-structured contracts, lien rights, and other legal protections to manage risk. We have already discussed several of these tools. Now we will focus on organizing separate business entities.

Legal Tools to Manage Risk

separate limited liability business entities

insurance coverage

contracts

lien rights or other security protections

Using well-designed business entities to separate assets from activities with higher potential business risk is key to ensuring the viability of the farm business and passing on the maximum value of the business to the next generation in the succession process. In addition, creating separate legal business entities can streamline the farm succession process by setting up clear rights, responsibilities, and expectations among everyone involved, even the nonfarming family members.

Every operation is unique and faces its own risks, but there are some common tools that help all farms manage those risks and help ensure their long-term business viability—namely, business entities with limitations on liability for their owners called “limited liability business entities.” It is important to understand that despite the use of that term, limited liability business entities do not necessarily have limits on liability for their own actions. These business entities are used to separate business assets from personal assets so that business liability threatens only the business assets. Because this isn’t a comprehensive solution, maintaining insurance and taking other risk-management steps are still key.

A. Why Form a Business Entity under State Law?

There are two broad categories of business entities: those in which the owners have liability for business debts and judgments (sole proprietorships and general partnerships) and those that are able to provide the owners with some liability protection if constructed and maintained properly (LLCs, limited partnerships, corporations, and cooperatives).

Around 80 percent of Oregon farms and ranches are currently considered sole proprietorships or partnerships—which implies that many farms have not started their succession planning process.

Sole proprietorships are the “default” business entities that are formed if you just start doing business, and they have unlimited personal liability for business actions. If the business assets are owned and controlled by one person, it is called a sole proprietorship. This means that all the business assets are held in the owner’s personal name—the land, equipment, livestock, and so on—and all debts and contracts are taken out in the owner’s name. The business may have an assumed name that is used for marketing, but it does not give further legal protections.

General partnerships are similar to sole proprietorships, but the business assets are owned and controlled by more than one person. Again, all assets and debts are owned in the partners’ names, and each contributes personal assets to the partnership. Each partner is seen as an authorized agent of the business, which means that one business partner can sign a contract or loan or otherwise incur liability for the business without consulting the other(s), and all partners are liable on the debt. Business partners share everything—assets and profits along with liabilities and debts. Like a sole proprietorship, there is no separation between a partner’s personal assets and the business and its debts and liabilities, resulting in unlimited liability so that if a creditor sues successfully for a business debt, they can also get paid from the farm owners’ personal assets, such as bank accounts, vacation homes, or other personal property. While the advantage of sole proprietorships and general partnerships is that they are simple to form—if you own the assets and start doing business, you are governed by their rules—the disadvantage is that they do not protect your personal assets from business risks.

Operating a sole proprietorship complicates the succession process after the death of the owner and is likely to result in substantial loss of business value in the transition, even if a will or trust has been established.

Around 80 percent of Oregon farms and ranches are currently considered sole proprietorships or partnerships—which is a concern because organizing the business as a limited liability entity is a first step to business succession planning, implying that many farms have not yet begun the planning process. Operating a sole proprietorship complicates the succession process after the death of the owner and is likely to result in substantial loss of business value in the transition, even if a will or trust has been established. Transferring the ownership of each of the owner’s business assets to a new generation takes time and money and is not always structured in the best interest of the business.

Limited liability business entities separate the business liabilities from your personal assets (unlike sole proprietorships and partnerships). Separating personal assets from business liabilities is the primary reason for creating a limited liability business entity. Transforming your farming operation into a limited liability company (LLC), for example, involves filing articles of organization with the Oregon secretary of state, using the appropriate forms, creating an operating agreement, filing the new entity with other regulatory agencies related to such things as taxes and employment, and operating the business according to the rules. The important distinction is that the business is recognized as its own legal “person” in the eyes of the law. It is separated from your personal assets. Unlike a general partnership, owners of the LLC cannot make decisions on behalf of the business or other owners unless they are authorized to do so in the operating agreement. The business entity can own property, enter contracts and loans, sue, and be sued. The business entity stands in the place of the business owners. Therefore, if the business is sued or defaults on a loan, the business and its assets carry the burden of the risk, not the owners.

Of course, the owners put their investment in the business, and that investment is at risk. No entity operates behind a perfect magic legal shield; people can still sue the business for debts and liabilities. But if operated correctly, it limits the owners’ liability to the assets that they have invested in the business. When done right, and without the presence of other circumstances leading to an owner’s personal liability, it provides some protection for personal assets in lawsuits or other claims. Your business lawyer may advise that you would be better off setting up your farming operation as an LLC because a shield, even if not bulletproof, is better than no shield when you are being sued.

B. Choosing a Business Entity

Every business operates within the legal rules of the county, state, and federal government. The types of entities available to form a business and their primary characteristics are established by the state. The state also creates and enforces the laws regarding contracts, loans, property, and torts.

Four characteristics to consider when choosing a business entity:

Liability of owners for business debts

Taxation

Owners’ rights, such as decision-making and profit-sharing

Ease of administration and succession

In short, you should choose the business entity available in your state that carries the right mix of limits on an owner’s personal liability for business debts and judgments, minimizes taxes when moving assets around, maximizes your ability to control the business, and is manageable to administer while facilitating your ability to pass the business on to the next generation. Only a skilled business lawyer familiar with you, your business, and your goals and aspirations can advise you on the correct business entity for your purposes. Here we will discuss some of the choices available in Oregon with the hope that this information will help you ask questions of your legal, tax, and financial advisors and understand the implication of their recommendations as you make the right choices for your family and business.

Most lawyers will begin by pointing out the need to organize the farming operation as a form of business entity that will separate its actions and other liabilities from the owners’ personal assets and the farm’s hard assets, like land or livestock. This will provide some protection from liability to its owners. No business organization can provide perfect separation or perfect limitation of liability for the owners. It’s a risk management tool, not a risk elimination tool, and there is no perfect solution. Further, improper business formation and lack of careful maintenance can erode even the most basic aspects of separation and liability protection. Everything must be set up and maintained correctly for the owners to enjoy the benefits of business organization.

Key legal advice: separate the farming activity from the ownership of land to protect the value of the land from legal judgments that arise from farm operations.

That said, most business lawyers will begin by advising the farm owners to separate the farming activity from the landowning activity. The simple goal is to place a barrier against liability between the entity with the greatest likelihood of injuring someone and the entity that owns the farm’s most valuable asset—land or cattle. Therefore, the typical first step in a business succession plan is to get the farming operation itself—the activities of buying, selling, farming, hiring, and so on—into a separate organization from the farm’s hard assets, such as the land, and the owners’ personal assets.

Here we will discuss the characteristics of LLCs rather than corporations or other limited liability business entities. We will analyze the LLC in the context of the four main goals for choosing a business entity previously discussed. There are other entities available that offer limited liability, but these vary in their tax requirements and other implications; they are corporations, limited partnerships, and even nonprofit corporations, which your operation could be qualified for if it had a charitable purpose. Corporations, for example, are much less flexible than LLCs and so are rarely used unless there is a high operational risk, such as selling food directly to the public. Currently, most for-profit family farms seem to be choosing the LLC to organize their operations, so we will focus on that in this guide (see table 3 for LLC terminology)

Table 3. LLC terminology and characteristics

Name

Farm Name LLC

Owners/investors

Members

Who makes management decisions?

Managers or members (depending on whether a manger is hired who is not also a member)

Creation document

Articles of organization filed with secretary of state and $100 fee

Governing document

Operating agreement

Owner’s investment

Capital contribution

Ownership share

Membership interest defined in terms of a percentage

Payment of profit to the members

Distribution

Payment of a salary to a member

Guaranteed payment

Are members personally liable for LLC debts or judgments?

No. Liability for business debts and judgments are limited to a member’s capital contribution if LLC integrity is maintained. In Oregon, a judgment against an LLC results in a charging order against LLC distributions.

Can a creditor have a legal claim on a member’s personal assets?

Not usually, but creditors may “pierce” the LLC veil if members comingle personal and business funds, do not follow legal requirements for the LLC operation, or undercapitalize the LLC.

How many members can an LLC have?

One or more; can be individuals, other business entities, or trusts

Are annual meetings required?

No

Is there ongoing reporting to the state?

Yes, you must appoint and maintain a registered agent who has a physical street address in Oregon and fill out a renewal form with the basic LLC information (name, registered agent, member names, etc.) with $100 fee. Due on the anniversary of formation.

How are LLC profits taxed?

You can elect the pass–through method of taxation: members file and report the LLC’s income on their own separate personal income tax returns based on percentage membership interests owned. If you do not elect pass-through taxation, the LLC is double taxed: once on its profits and again for each member.

C. Forming an LLC

The legal formalities of starting an LLC are relatively easy—just fill out and file articles of organization with the Oregon secretary of state, pay a small fee, and capitalize the LLC by moving existing farm assets into the LLC’s name. You should also create an operating agreement for the LLC.

The articles of organization can consist of a simple form supplied by the Oregon secretary of state’s office. In it, you report the basic information about the LLC, register an agent to be served in the case of a lawsuit and a person and a place to receive official LLC mail, and pay a fee. In 2019, the filing fee for the articles of organization was $100. Then you will file a renewal form every year on the anniversary of the LLC formation with the same basic information (updated if necessary) and a $100 fee.

The operating agreement defines the rights of the LLC members (owners) and managers. While there are default state rules that govern the relationship between LLC members, it is wise to also create your own operating agreement. Writing an operating agreement that considers the unique complexities of your family and farm business takes some care and attention. After thinking about the options, you can use the help of an attorney to craft the right operating agreement for your situation. For example, in a multigenerational LLC, it is important to clarify who has management control, what members without management rights can vote on, and how votes are counted. It is also wise to set the rules for LLC distributions so that there is no confusion down the road. To keep the LLC in the family, there should be buy-sell agreements for all member shares, so that if a member wants to leave the LLC, they must sell their shares within the family or the LLC can buy them out, with a valuation method and payment schedule defined so that a departing member does not drain the LLC of operating cash. Family members can also decide in the operating agreement the procedures for dissolving the LLC if they decide to liquidate the business.

While there are no annual meetings or formal recordkeeping requirements as with a corporation, it is wise to have meetings and keep excellent records of decisions to protect the LLC member-managers if other members are unhappy with the business direction at some point in the future. It’s also just a good idea to keep track of the decisions that have been made by the business.

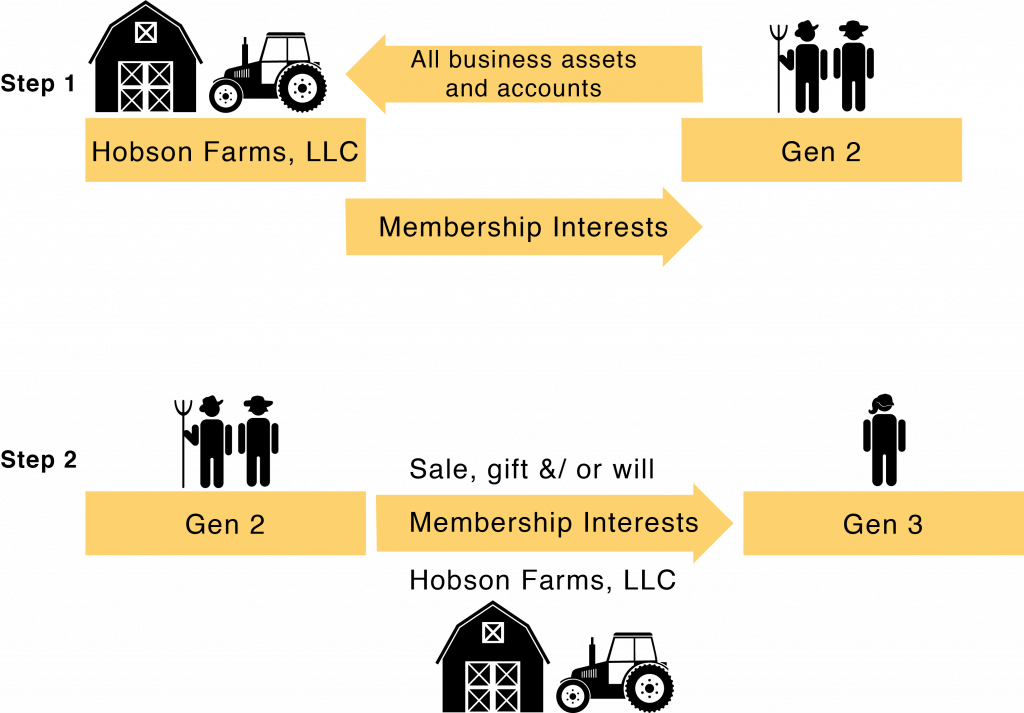

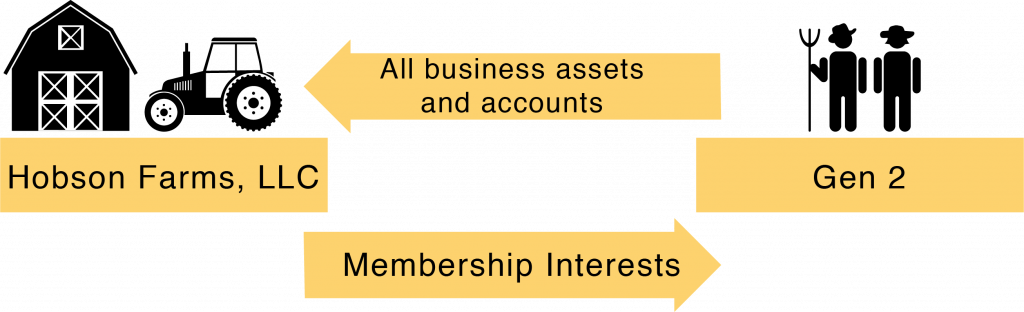

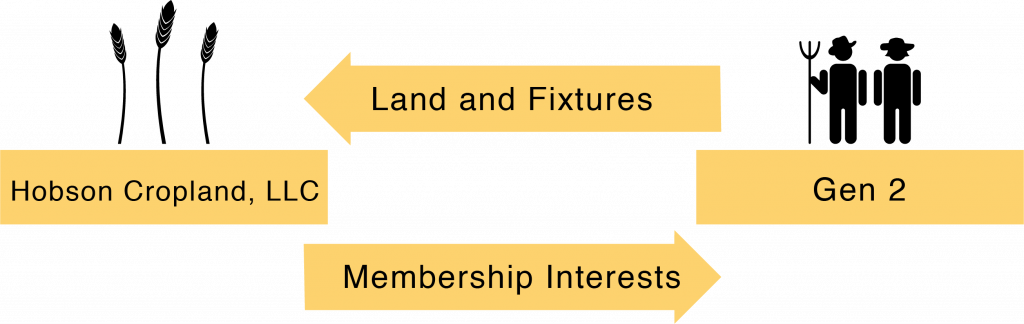

Capitalizing the LLC from an existing farm business involves moving farm assets from Gen 2’s personal ownership to LLC ownership, which represents their capital contribution to the LLC. In exchange, Gen 2 owns all the membership interests in the LLC (figure 4, step 1). Gen 2 can then gift or sell membership interests to other people, including family members, immediately or over time (figure 4, step 2).

Figure 4. Capitalization and ownership of an LLC

D. Operating an LLC

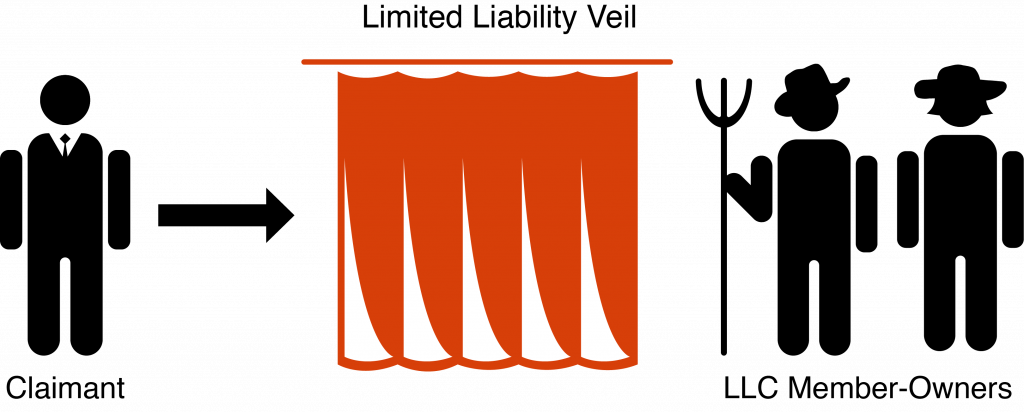

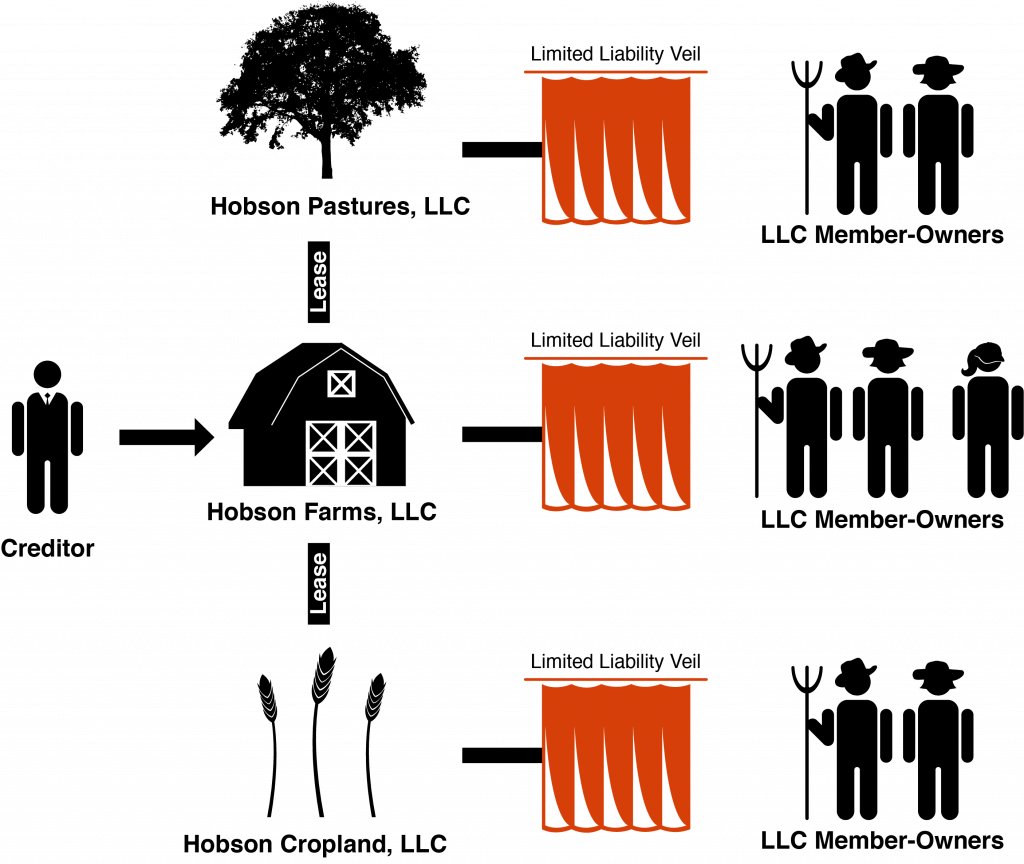

The limited liability veil of the LLC can be “pierced” if the business is not operated as a separate legal entity, such as keeping separate accounts for business income and expenses. If you comingle business and personal funds, such as using business funds for personal expenses, you could also be personally liable on the debts or liabilities of the business.Operating the business as its own separate legal entity is one of the keys to maintaining the limited liability aspect of an LLC. If someone sues the business, they may “pierce” the limited liability veil of the LLC and go after the owners’ personal assets if they can prove that the business was not operated as a legal entity that is separate from the individual members of the LLC (figure 5). This exposes the owners’ personal assets to full legal liability for business debts or judgments. The business must have adequate capital to engage in certain functions, such as paying its monthly bills and loans, buying inputs as needed, or paying for other expected expenses. For example, if the business takes on more debt than it can reasonably pay off with expected revenue, the LLC will be considered undercapitalized.

Figure 5. The limited liability veil

In addition, business accounts must be kept separate from personal accounts. Business accounts cannot be used for personal expenses. The business can pay reasonable wages and bonuses to employees, who may also be owners, and profits may be distributed to owners as well. Therefore, it is critical to keep the business assets and accounts separate from personal accounts and maintain proper accounting and business records.